Fintech 🧠 Food - Mar 14 2021 - Pipe.com raises $50m, BlockFi $350m and why annual budget cycles have a lot to answer for

Fintech 🧠 Food - Mar 14 2021 - Pipe.com raises $50m, BlockFi $350m and why annual budget cycles have a lot to answer for

Hey everyone 👋, thanks so much for coming back for more Brainfood. A space to learn in public and hopefully process everything happening in fintech.

If you want to join the 231 new subscribers since last week, you can right here. 👇

Episode 1 of Under the Hood, the NEW 11:FS podcast, is here!

We've created this 10-part podcast series with our friends at Synapse - it's all about how fintech really works under the hood. Want to take a look? 👀

Tune in to episode 1 now 👉 Click here

Weekly Rant 📣

The tyranny of annual budget cycles

JP Morgan closed ChasePay, after spending a reported $100m. Banks have the R&D budget to innovate, but it's not how much they're spending that's the issue; it's the annual budget cycles, desire for in-year return, and the default to using the wrong metrics for a growth product.

So if we know this, why isn't it changing?

Three reasons

1. Annual budget cycles

2. The psychology of change

3. Which is causing tech debt to compound

The tyranny of annual budget cycles 🚲

Most banks run in annual budget cycles. August to September becomes a key time to start making budget asks for the following year. 80% of the budget is immediately assigned to "compliance / mandatory" change, with the remaining 20% average for product innovation. From here, there are two types of work.

A) Last year's work continues. Large multi-year programs securing another year of funding to do things like continue to add features to the mobile app.

B) New initiatives. For those of you that work in startups, these new initiatives are not what you expect. They're either hard-won by the product team, or more likely, they're a result of lots of work from strategy teams. Strategy consultancies do lots of PowerPoint, looking at the market before concluding they need to do exactly what everyone else is doing. If it's a user-facing change, it is likely handed to an external design agency to crank out some UI screens. If the change is not user-facing, consultancies, systems integrators, and an absolute army of internal IT teams set about estimating and creating architectural designs.

The psychology of change 🧠

The business case is predicated on driving an in-year return for investment. Therefore, the delivery date must be in-year, which creates a complicated air-traffic control problem for project and program managers' armies inside the bank. Resource allocation is hotly debated in funding and governance forums.

The battle is for what feature gets to be on the roadmap, not whether that feature will be any good.

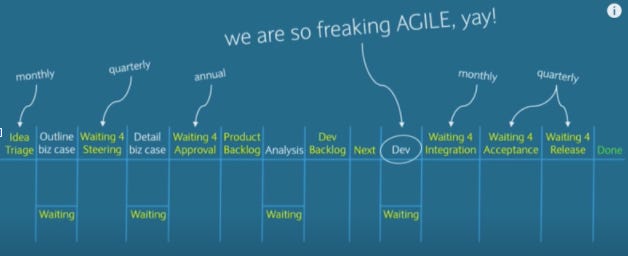

In incumbents where change meets funding or any of the various risk forums, that process is far from agile (or agile at scale); it is exceptionally waterfall. Yet incumbents spend hundreds of millions with strategy consultancies to try and deliver "agile at scale." The problem with these "agile at scale" programs is they're all focused on the symptoms, not the cause.

Tech debt compounding 📉

Most often, it's not the engineering team that the issue, writing code is incredibly efficient, most incumbents are using modern tools and modern practices, but they're waiting for other teams, other governance forums, or processes. What's more, the engineer has zero autonomy to find a better solution to a problem. Much work has been done and time spent, political capital spent that the tech team must deliver the functionality.

Because incumbents consistently set the roadmap annually, choose the fastest time to market, and the process of delivery is anything but agile. Despite this, there are good efforts to make the architecture more modular, CIOs are trying to put in place standards. They're just not succeeding because power is in the budget cycle.

This means many new deliveries compound the previous tech debt. The imperative for in-year return is preventing banks from creating a tech estate that can be digital. This isn't the fault of the technology teams; it's the bean counters.

You can't have Spotify-style governance if your budget cycle is annual.

You can't have Square-like user and earnings growth if your only metric is in year return.

You can't have nice things if you don't fix the bean counters first.

If you're wondering, where is the customer in all of this?

Me too.

4 Fintech Companies 💸

1) Rail - Pipe.com for Europe

Rail provides revenue-based finance for SaaS businesses (like Pipe.com). SaaS business founders connect their billing system and share their data with Rail, who will then offer a cash payout secured against future revenue. Unlike revenue-based finance for e-commerce businesses, SaaS revenue is much less reliant on advertising. A SaaS business's data shows its net revenue retention, and as an underwriting metric, this scales much better than e-commerce advertising conversion.

This service's need is higher in Europe, where venture debt markets are far less mature than in the US (or in countries like Poland nonexistent). Like pipe.com, Rail's vision is to build a two-sided market where institutions can buy revenue-based finance.

2) Wrapbook - Payroll for TV & Film

Wrapbook simplifies payroll for TV, film, and commercial productions. Entertainment payroll is difficult to track as cast and crew move from project to project. Wrapbook manages all of the tracking of payments and insurance. Wrapbook expects their solution to apply to other project/freelance industries, but entertainment has a strong wedge for them.

"Payroll for X" is an interesting category. There are several industries where the jobs to be done overlap between accounting, figuring out who needs to get paid, and ensuring all of that happens on time is a major headache. Vertical SaaS for fintech will keep churning out hits as this "where money meets other admin jobs" space is 0.1% done, and there's so much value there.

3) Debie - Credit underwriting automation SaaS tool

95% of credit processes require some manual work. Debit offers instant reference checks, court filing checks, and integrated KYC / AML. Debie is designed to integrate into existing ERP and CRM systems without developing a custom / new solution in the corporate IT stack.

The alternative to something like Debie is to wholly outsource an entire business line to a SaaS platform (e.g., Blend.com for Mortgages). That has some advantages because it is comprehensive in running the product lifecycle from front to bank. For other groups that either don't want to outsource wholly or have heavy integration needs, smaller point solutions like Debie could add real value without moving a large % of the IT systems to a 3rd party. An interesting question for bank CIOs, how atomic do you want your SaaS supplier to be and why?

4) Cheese - Banking for Asian America

Cheese gives up to 10% cashback, a 3% deposit bonus, and a "giveback" program for Asian charities and businesses. This is in addition to now-standard Neobank features like getting paid earlier. Cheese solves some specific challenges for Asian immigrants, like not getting credit or not having services in your first language.

Following First Boulevard last week, Daylight, Greenwood bank focuses on communities not in geographies but with a common connection digitally. The founders have lived the experience they're aiming to solve and have been able to use the combination of modern BaaS tools and their cultural insight to build something with a unique appeal.

Things to know 👀

1) Pipe raises $50m to be the NASDAQ for revenue

Pipe.com provides SaaS companies with funding outside of equity or venture debt. Pipe pairs early-stage SaaS companies looking to get their revenue upfront with a marketplace of investors who pay a discounted rate for those contracts' annual value. Pipe's round includes Shopify, Slack, Hubspot, Marc Benioff, and Chamath Palihapitiya. "Buzzy" probably just about covers it.

Pipe is looking to move beyond SaaS companies to "any company with a recurring revenue stream" with its funding. Pipe (like Clearbanc or Uncapped) integrates with accounting, payments, and banking systems and provides a real-time performance rating. Where Pipe differs is they have a two-sided market. Pipe is essentially a trading venue for a new asset class recurring revenue. As a marketplace, Pipe has no cost of capital, instead of charging both sides 1%.

🤔 My Analysis: Recurring revenue has been the engine of growth for SaaS in the past decade. Perhaps the best case study of how powerful recurring revenue has been Adobe moved from 3% SaaS revenue in 2012 to 88% in 2020. In that time, their share price moved from $35 to $350, and average annual PBT growth has been 20%. Businesses with ARR massively outperform other business models.

🤔 My Analysis: Three things have come together for Pipe.com's model to be quite so interesting. 1) VCs have developed a standard set of metrics to quickly evaluate any SaaS business (annual recurring revenue, net revenue retention). 2) Accounting tools like Quickbooks, Billing tools from Stripe, and services such as Plaid make real-time performance data available and future potential income. 3) Investors and founders have increasingly tried to build two-sided marketplaces (from ride-hailing to Amazon and back).

🤔 My Analysis: The secondary market is elegant because investors are hunting for yield. This is, in theory, how "P2P" lending ended up, where investors bought most of those loans. Over time, P2P lenders have become much more traditional lenders and less marketplace-driven, but I think there's something different with Pipe. The data and risk model. Pipe has innovated on the data like Clearbanc, but unlike Clearbanc, it created more of a marketplace. Moving beyond SaaS will be hard though other sectors don't have predictable income flows, which makes SaaS so appealing.

2) Crypto wallet Blockfi completes $350m Series D

BlockFi, arguably the most famous and popular lending and multi asset based wallet, has raised $350m (at $3bn valuation) to build a bridge between crypto, traditional finance, and wealth management. BlockFi's core offering for consumers is earning yield on cryptoassets at attractive rates, buy/sell/hold cryptoassets, and, importantly, originating US dollar loans secured against the cryptoassets on the platform. For institutions, BlockFi is a lender and trade execution provider.

BlockFi was one of the first wallets to offer a Visa rewards credit card linked directly to underlying stablecoin holdings. For example, I could hold USDC / USDT in my BlockFi wallet and spend directly from that balance using the BlockFi debit card. BlockFi has more than 225k users, monthly recurring revenue is more than $50m (!!), with more than $15bn assets under management (AUM).

🤔 My Analysis: How long until we see Payroll companies like Gousto adding USDC / USDT payments to crypto wallet addresses? If I were a well-funded wallet provider pushing towards direct deposit would be well worth exploring.

🤔 My Analysis: This DeFi wallet is worth almost 2x Monzo, but crypto is probably a fad 🙄. I'm being slightly glib; in the week where Bitcoin hit $60k (at the time of writing), crypto could well be in another stimulus-funded bubble. But it's also here to stay.

Quick hit:

Digital mortgage broker Habito launched a 40-year mortgage in the UK. This is interesting for younger folks who can't get a deposit given ever higher asset prices and something you'd never see from a traditional lender. Habito also started as a broker before getting into lending. Despite its small balance sheet in 10 years, I expect them to put a major dent in the UK market where super low-interest rates and lenders are squeezed.

It's been a busy week in fintech! If you missed any of it, check out Nik Milanović's This Week in Fintech for the headlines of the past week.

- Plaid launches a new returning user experience.

- Mastercard launches a card to reward shopping at women-owned businesses.

- Nium expands in Africa.

- HSBC offers banking to the homeless.

- Chase is winding down Chase Pay.

- Big fundraises from Starling, Flutterwave, and M1 Finance.

Good Reads 📚

1) Interview with Patrick Collison

There's so much here it's hard to do this interview justice, but here are some points that stood out.

Outside of modern software, much of the US and Europe's infrastructure has a high install base and is hard to "meta-maintain." Financial services are the perfect example; the only "enemy" is the installing base's calcification.

"Most systems get worse as they scale," and states and local government are other examples where the systems become too rigid to change. Patrick also gives the example of the FAA, which in its early days enabled a successful innovation sector with clear rules for air space, air traffic control, and airports). Today with more than 45,000 employees, it can be tough for the industry to get innovations like electric engines approved because of the expense and sheer amount of paperwork. There's almost no lobby opposed to electric engines; they're likely to be legalized at some point; there's just a big status quo bias.

🤔 My Analysis: This is a must-read for regulators or anyone designing policy. Regulation and law are such powerful tipping points in a national or global system. By re-balancing these tipping points, we can create massively beneficial outcomes for society. The UK's FCA started a trend with the regulatory sandbox and is now pushing the boundaries with its "digital sandbox" and looking at data-driven regulation. For me, this is still dabbling.

🤔 My Analysis: This report from the UK Government Office for science in 2014 is where the reg sandbox trend started. It recommended a "clinical trial" methodology for financial innovation, which became the regulatory sandbox. I think the metaphor we're looking for is modern software engineering practices. How do we view the financial (and other systems) as a collection of primitives (microservices) and build massive redundancy with horizontal scaling that increases experimentation? Reach out to me if you want to chat on this. I love systems with tipping points :)

2) Roblox is a company to understand better

Byrne describes Roblox as "a modable videogame whose usage consists almost entirely of mods, where the audience is under 12". Roblox players have custom avatars that interact with a town, school, pizza place, etc. Players pay to access unique locations and for custom, avatars using an in-game currency called Robux. Roblox reported $589m revenue in Q1 21 but 68% YoY, but their revenue recognition understates who much money customers are paying today. Because Roblox, under GAAP, has to recognize any purchase over two years, their bookings in Q1 are much more interesting (at $1.2bn, up 171%).

Byrne describes how developers do not always cash out Robux to real-world currency; some choose to invest it in developer tools, promote their experience, or spend as any other user would. In other words, Robux has a share of its expenses denominated in a currency it can print. This is an early virtual economy. Roblox aims to grow its services as its audience ages. The product experienced by users is constantly changing; as long as Roblox can keep its servers running, it can keep collecting its cut.

🤔 My Analysis: Compare this to GTA5, with an army of developers crafting experiences for its audience. Roblox is well-positioned to grow a new class of content creators and help them monetize inside its platform.

🤔 My Analysis: If you haven't read up on the Open Metaverse concept, now might be a good time to do so. Where Roblox is a closed platform, imagine a world where creations can move between different IPs. Your creation in Roblox could appear in Fortnite; you could sell your Minecraft artwork in online galleries. This is still frontier stuff, but you should jump into Decentraland. It has that using the internet in 1993 vibe, which makes it a great time to learn.

Bonus reads

3) Marc Ruby with a full rundown of what happened with Greensill

4) The incredible Ankit Singh on what's coming next with Embedded Finance

Tweets of the week 🕊

That's all, folks. 👋

Remember to share if you love this content, it helps other people find it.