Fintech 🧠 Food - 18th July 2021 - Revolut's unique path to $33bn, Square's Bitcoin unit is TBD & Apple Pay Later

Fintech 🧠 Food - 18th July 2021 - Revolut's unique path to $33bn, Square's Bitcoin unit is TBD & Apple Pay Later

Hey everyone 👋, thanks for coming back to Brainfood, where I take the week's biggest events and try to get under the skin of what's happening in Fintech. If you're reading this and haven't signed up, join the 6,834 others by clicking below, and to the regular readers, thank you. 🙏

Are you excited about where Crypto meets Fintech? This week 11:FS relaunched Blockchain Insider, with a new episode all about Stablecoins. You can check it out here or wherever you get your podcasts :).

Weekly Rant 📣

Revolut's unique path to $33bn

With $308m of FY20 revenue, that's over a 100x multiple. Put another way, with their $6.4bn of deposits, it's 5.1x their entire deposit base. This is a frothy valuation even by Fintech and 2021 standards. It's not surprising the round has been led by Softbank and Tiger Global, but what's the story here?

Is Revolut for real?

Revolut appeared in the cohort of "challenger banks" in the UK in ~2015 alongside Starling and Monzo. While Starling and Monzo secured a banking license, Revolut has not secured a full UK banking license (although it has one in Lithuania).

Revolut began life simply as a debit card with the best FX rates in the world. It is now one of the contenders for "financial super app" with ~15m users in 30+ markets and a valuation higher than Brazil's NuBank.

On 11:FS Pulse (the video database of user journeys), Revolut user journeys are consistently among the most viewed videos. Their UX is a benchmark and best in class.

Revolut then Blitzscaled.

The move fast and break things approach may be why they don't yet have a full UK (or the US) banking charter, but I think this has worked out to be a feature, not a bug.

Getting a license is hard; keeping it is harder. Once Monzo got its full banking license, its growth slowed, its feature velocity slowed, and it started to miss a step. Revolut, by contrast, has increased its momentum, feature velocity, and scale in the same period.

Rather than using its deposits base to lend against, Revolut has been forced to find other paths to growth and revenue.

Revolut has scaled its product breadth rapidly. Revolut was the first Neobank outside the US to offer Crypto or stock trading. They moved into the subscription/metal cards before other Neobanks

Revolut has scaled Geos faster than most. Operating in the 31 EEA markets, plus Japan, Singapore, Australia, Switzerland, and the US - I'm hard-pressed to think of a competitor that has their breadth.

Revolut has scaled out the customer type they serve. Their consumer audiences have widened. Revolut started with the prosumer/traveler in Europe but is now widely used as a mix of Coinbase, Robinhood, and Wise. They've expanded into SMB offer a mix of multi-currency accounts, card and expense management, global FX, and subscription management.

Revolut is rebundling fintech.

If you remember that slide of Wells Fargo's homepage with all the Fintech companies unbundling them. Someone should do a version of all of the Fintech companies Revolut can (technically) compete with.

Blitzscaling brings haters.

Revolut has been accused of having weak compliance and anti-money laundering controls, with the UK Regulator, the Financial Conduct Authority conducting an investigation in early 2019.

During that period, former employees reported a culture of growth at all costs, unachievable goals, and high staff turnover. Initially, CEO Nik Storonsky had been unapologetic about the performance and hard-working culture before adopting a softer tone.

Revolut also made some miss-steps in its advertising, with a now-infamous poster from 2019 that read "to the 12,750 people who ordered a single takeaway on valentines day, you ok hun?" Aside from being a bit mean-spirited, the Neobank appeared to be using personal data for advertising purposes (something it was later cleared of).

Perhaps most strikingly, Lithuania's central bank looked into alleged connections to the source of investor capital with the CEO's potential links to Russia. (But then issued a license)

Revolut has taken steps to strengthen and grow its AML tooling and team; it assured the regulator it didn't break PII (personally identifiable information) rules. In recent years it has brought in tenured senior bankers to help scale the organization beyond its initial hustle culture.

But Revolut remains a rorschach test. What you think of them says as much about you as it does them.

Is Revolut the shady dealing, growth at all costs pariah? Or is it an inspiring, blitzscaling Neobank that had some growing pains but is delivering results?

Something is working; Revolut is delivering numbers.

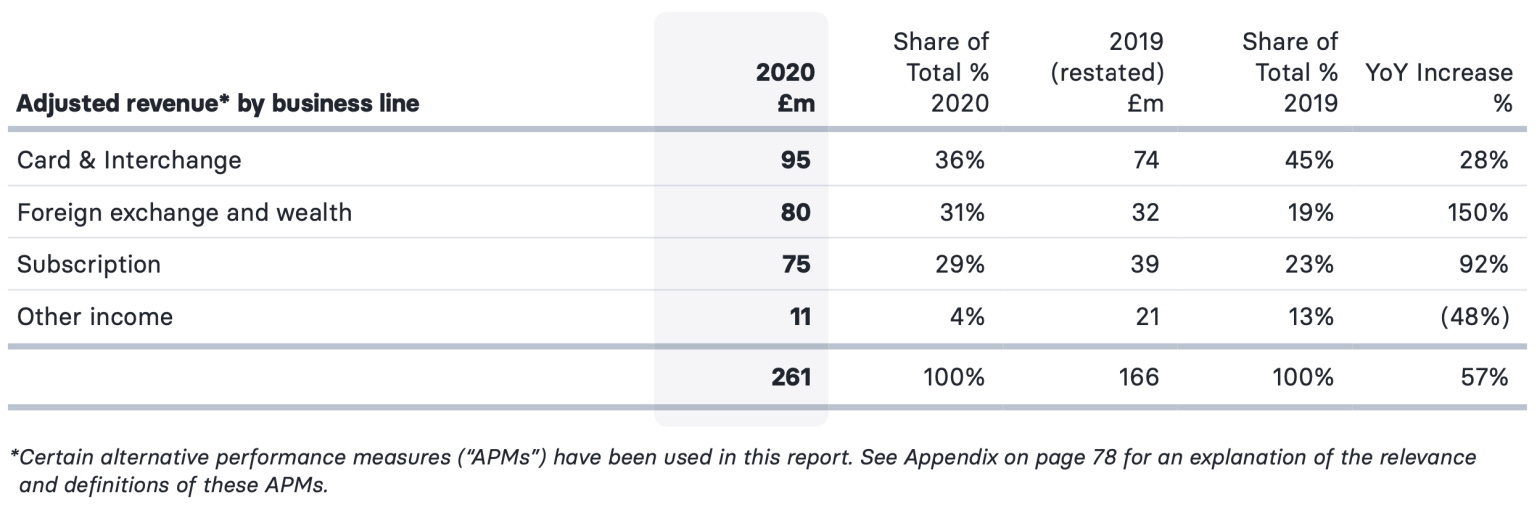

Revolut grew revenue by 57% through 2020, helped by Crypto and new features like stock trading, increased subscriptions, and deepening their SMB customer base.

By the end of 2020, Revolut reported 14.5m consumer customers and an impressive 500,000 business customers. Revenues are split relatively evenly between Interchange, FX, and Subscriptions.

It was widely reported that 88% of revenues were from UK customers (making Revolut seem very UK-centric), but post-Brexit EU customers are no longer served out of their UK e-money license. The actual customer split is closer to 4m consumers in the UK and ~10m across the rest of the European Economic Area (EEA).

Soft Bank and Tiger Global are buying into a blitzscaling, customer acquisition machine. But there are some threats on the horizon.

But there are many unanswered questions.

How the heck can they justify that valuation? Softbank is not afraid to make wild bets. Sometimes it wins big, sometimes it loses big. For every WeWork, there's Flipkart. Softbank (and Tiger) are betting on momentum. Revolut's stated aim is to grow users and become profitable later. This worked for Jeff Bezos and Amazon, but eventually, it has to hit profitability somewhere down the line.

Maybe like Amazon, Revolut finds a cash cow product like AWS.

Or perhaps they never really hit profitability and become a growth mad, low margin business that has to pivot (like Uber).

Maybe all of these consequences play out after they exit, and maybe that's some other investor's problem?

Does Revolut have an engagement problem? Blitzscaling can often lead to high churn and low daily active use (DAU). Revolut apparently had a 1.1m DAU rate in 2020, which is the exact same as Monzo (who has 1/3rd the number of customers). Robinhood sees nearly 50% daily active users.

If they're going to hit profitability, they're going to need an engaged customer base.

Can Revolut break the US? The US is a highly crowded Fintech market and not just in Neobanks. Every corner of the consumer and SMB Fintech sector has well-funded category leaders with their own astonishing momentum.

My sense is Revolut may have more joy outside the US than in it. There is a gap in the market for the non-US, non-Chinese Fintech super app, and Revolut is well placed to be it.

Is Revolut fighting on too many fronts? Blitzscaling has a cost; Revolut can dominate some Geos and some segments, but it's harder to dominate all the Geos and all the segments.

Where does Revolut stop? Do they know when to?

The Revolut has begun.

Their opportunity is vast; if there's one company currently in the lead when it comes to rebundling Fintech (outside the US), you'd have to argue that is Revolut. There are Fintech companies deeper in their home markets, with higher revenues and even higher growth. But there's only one Revolut.

The worry about Revolut will always be whether it can tread the line between move fast and break things vs. move fast and break rules.

The big question is what happens after IPO. Will we see high churn? Is it just being built for a big exit? Or is this something that can shake off its growing pains and become a financial super app?

The lesson is that being something other than a bank is a great place to build Fintech products. But I'd like to see more balance between the functional utility (this product solves a problem) and social utility (and leaves the world a better place in the process).

ST.

4 Fintech Companies 💸

1. Coincover - Insurance and Key Management for Crypto

Coincover ensures investors are protected from fraud, theft, or hacks by combining secure private key backup with traditional insurance products from Lloyds of London. The deposit protection guarantee covers up to $1m in Crypto should a provider fail or suffer an outage. Customers include Bitgo, Curv, and Fireblocks.

As mainstream institutions look to enter Crypto, having high tech and traditional insurance can be a compelling combination. Crypto is still the wild west, and if your op-sec isn't cutting edge, hacks and fraud are a significant risk.

2. Crypcentra - Bloomberg for Crypto

Crypcentra has built tools to help investors collect and analyze data to help meet their investment goals. The platform can screen for assets that meet specific criteria, monitor pricing, and arbitrage opportunities, and view multiple exchange order books in a single dashboard.

I had no less than four different people ask me for an intro to Crypcentra this week, something in the water with these guys. There are many pure data tools and dashboard providers (e.g., coinmetrics or skew (acquired by Coinbase)). What makes Crypcentra stand out is the design-led approach to what a trader is trying to achieve. They've moved up the value stack from offering pure data, filtering the noise, and presenting the trader's data, which the trader can actually use.

3.Gregfins - If Transferwise and copilot.money had a baby (UK)

Gregfins provides an international overview of your finances for global citizens. Through a single app, users can choose the right card for the best FX rate at a given time. Gregfins aggregates multiple bank accounts across Europe initially, with the intent of covering every market that has open banking capability.

The "account for global citizens" and banking like a local is something Wise innovated and is a niche not yet fully explored. The Gregfins build is PFM and managing money more effectively. A company in the UK called Curve combines many cards into a single card (so you can get lower FX and still get those air miles). If Gregfins added the multi-card through a single card capability of Curve, you'd have a genuinely global account.

4.BrightID - Crypto native identity

BrightID provides proof you are a unique human without requiring personal information. BrightID verifies its users based on their existing social connections and the communities they belong to. The first verification level involves joining a "connection party" where some evidence of you being a human is proved to other humans. BrightID then uses "social recovery," where users choose 3 people they really trust who can help re-set their account should they change device or suffer a hack.

BrightID has been popping up as the default way to verify yourself (over and above connecting a crypto wallet) in several exciting projects in recent months. In Crypto, you want to have many wallet addresses (it's just good Op-Sec), but there's value to proving skills, experience, or track record. I'm a big fan of privacy-preserving technology that can still help us manage risk. You could imagine a world in which linking your BrightID allows you to prove you are not involved in any suspicious transaction patterns while maintaining your individual privacy. This could be more effective than our existing, outdated AML framework.

Things to know 👀

1. Square is creating a new Bitcoin focussed business unit.

Square is building an open developer platform on top of Bitcoin to make it easy to create decentralized financial services. The entire platform will be completely open-source, like Square's previously announced Bitcoin hardware wallet.

🤔 My Analysis: In essence, Square is building a sort of Stripe on top of Bitcoin. Another way to think about it is sparking a Defi ecosystem on Bitcoin (which already exists but isn't as popular as the Ethereum ecosystem).

🤔 My Analysis: Square is leaning into several macro trends at once. Money as culture, the rise of the creator economy, and the decentralization of money. With their Tidal acquisition, consumer and merchant networks, and now Bitcoin unit, they're well placed to create another payments rail. Except now it's composable and permissionless.

🤔 My Analysis: It stands out immediately that this is not built on Ethereum. Given the adoption of Bitcoin specifically in LATAM and developing economies and Jack's attempts to spend more time in Africa, I wonder if the goal here is more international than domestic?

🤔 My Analysis: Square has a history of making bets and being patient. Cash App took a lot of patience to get to market and even more for profitability. Square is also always flawless in execution. If anyone can make hardware wallets mainstream, it's Square.

2.Apple Pay is launching a Pay Later service partnering with Goldman.

Apple has announced the launch of a pay later product. Users will be able to pay for any purchase using Apple card in installments. This will apply to all merchants, not just Apple. When making a payment, users will be given the option of making 4 installment payments every two weeks.

🤔 My Analysis: This is very different to Affirm or Klarna. Those businesses would allow you to begin a BNPL at the checkout (i.e., from the merchant side); Apple is doing this whenever a consumer uses Apple Pay. This is an essential distinction because BNPL makes money by offering "0% interest" to the consumer by charging the merchant. Apple will likely have higher interest rates or need to build out increasing merchant partnerships.

🤔 My Analysis: For Apple, financial services are a vital area of growth. They are positioned well with high-earning, high spending consumers and can create beautiful experiences. Having installments as an option baked into every payment could be very compelling and sticky.

Quick hits 🥊

The European Central bank has announced its project to prepare for a Digital Euro. The project will build prototypes and also focus on legislative changes that might be needed. The project will also look into the balance of "privacy vs. anti-money laundering." 🤔 The ECB has three motivations, 1) The Chinese DCEP, 2) Fear of Facebook, 3) The belief that a digital euro "would be preferred" to crypto stablecoins. The first two make sense to me, the last one less so.

Employee expense management platform Ramp is adding the ability to create & manage cards for employees that block specific merchants. 🤔 Many other providers offer this kind of flexibility, but something about Ramp's execution is always 👌. Creating and managing these features is still too hard for companies like Ramp, even with modern payments processors. Very few processors make building this type of feature trivial. I sense that's because the answer one maybe two layers up. The ability to compose products out of data from various partners (like how payments orchestration is evolving) is largely missing from the market. It gets built internally by each fintech company. Some BaaS providers aggregate some of the Fintech APIs, but the ecosystem is still immature. There isn't yet an operating system for Fintech equivalent to Shopify OS.

Oh hi, you a regular? Why not go ahead and hit that subscribe button 👇

Good Reads 📚

Balajais suggested we're entering a world where everyone is an investor, and Robinhood's S1 filing would agree, "we're all investors now," it says. But maybe investor is the wrong word. Speculation exists in the gap between investment and gambling. Where an investment is purchasing an asset for the long term, speculation has a shorter-term time horizon.

Options trading lends itself to speculation. Fixed expiration makes them short-term, leverage increases the risk, and the upfront premium is equivalent to a gambling stake. For Robinhood, options are only 2% of transactions but 47% of their revenues. Perhaps we're all speculators now, or maybe we're in a speculative bubble, and Robinhood is exceptionally well placed to benefit.

🤔 My Analysis: Marc uses historic e-Trade data to show that in 2000, we saw a massive speculative bubble that consumers entered in a frenzy. But I think both things can be true, we're in a speculative bubble, and everyone is an investor now. Genies don't go quietly back into bottles, and the use of mobile-first design is far more accessible at scale to the mass market. Even if 75% of Robinhood's MAUs disappeared by 2022, my sense is by 2032, Macro trends would drive that number way back up.

🤔 My Analysis: Money is culture, investing is social, and opportunity is scarce. Asset prices are too high compared to earnings, real inflation is hidden, and Gen Y and Z will be working until they're 70 with very little retirement income and high student debt. Therefore, it's too hard for younger generations to build wealth without community support, access to riskier investment types, or earlier-stage investments.

🤔 My Analysis: Entrepreneurs have to tread the line between gambling and investment, between user interests and their own bottom line. That's why I believe, over time, the ones that build community are best placed. NFTs and DAOs are interesting for this reason; they're a peek at what community-driven asset management could look like (early, experimental, risky, but there's intangible magic there, like Defi in 2018).

Asking "Where should I keep my deposits?" is like standing in a crowded room with everyone shouting at you. Regulators push watermarks and trust, institutions the sense of protection, Crypto offers high APY, Neobanks a great experience, Robinhood the speculation and short-term returns.

The reality is deposits do different jobs, depending on who you are and your goals. They help you spend, speculate, invest, plan and save. You as an individual have different motivations, maybe you need to be engaged with your finances, or perhaps you prefer to automate, set, and forget. Fintech companies build a wedge for one of these jobs and create a "neighborhood" of jobs and products around their core audience.

🤔 My Analysis: I really like the way of thinking about the consumer audience here. Robinhood isn't for everyone, but it is for a lot of people. Thinking of consumer archetypes helps us escape our own observer bias as builders. What you find abhorrent and speculative may be just what a large part of the market wants.

🤔 My Analysis: The downside here is the human brain 🧠. We love variable rewards, and gambling mechanics can create bad outcomes for users. How do we ensure that we always balance user and business interests regardless of user archetype without introducing burdensome regulations?

Tweets of the week 🕊

That's all, folks. 👋

Remember, if you're enjoying this content, please do tell all your fintech friends to check it out and hit the subscribe button :)